Every business, regardless of its size or industry, must carefully monitor where its money goes. From day-to-day operations to strategic investments, understanding the nature and classification of costs is essential for maintaining financial health. Poor expense tracking can lead to inaccurate reporting, misinformed decisions, and strained profitability. On the other hand, clear visibility into different types of outflows allows businesses to optimize spending and improve overall performance.

In this blog, we will explore the meaning of expenses, differentiate them from expenditures, explain the difference between cost and expenses in accounting, and break down the types of expenses with real-life examples. We’ll also cover how to categorise expenses for more effective financial decision-making.

An expense is any outflow of money or resources that a business or individual incurs as part of their operations. Essentially, expenses represent the cost of doing business or running day-to-day operations.

For example, businesses incur expenses such as rent, utilities, raw materials, labour costs, or even marketing to keep their operations running.

Understanding the meaning is crucial for financial management. While some expenses are directly tied to revenue generation, others are simply required to maintain operations or comply with regulations.

Also Read: Understanding Accounts Payable: Definition, Process, and Examples

Understanding expenses is key, but it is also important to differentiate expenses from expenditures, as they are often confused in accounting.

While both expenses and expenditures involve cash outflows, they differ in accounting treatment and timing.

Now that we understand the differences between expenses and expenditures, let's delve into the distinction between costs and expenses, especially in the context of accounting.

In accounting, the terms cost and expense are often used interchangeably, but they have distinct meanings. Here's a breakdown of each:

Also Read: How to Calculate Marginal Cost: Formula and Examples

To manage and track these costs, it’s essential to understand the various types of expenses that a business may incur.

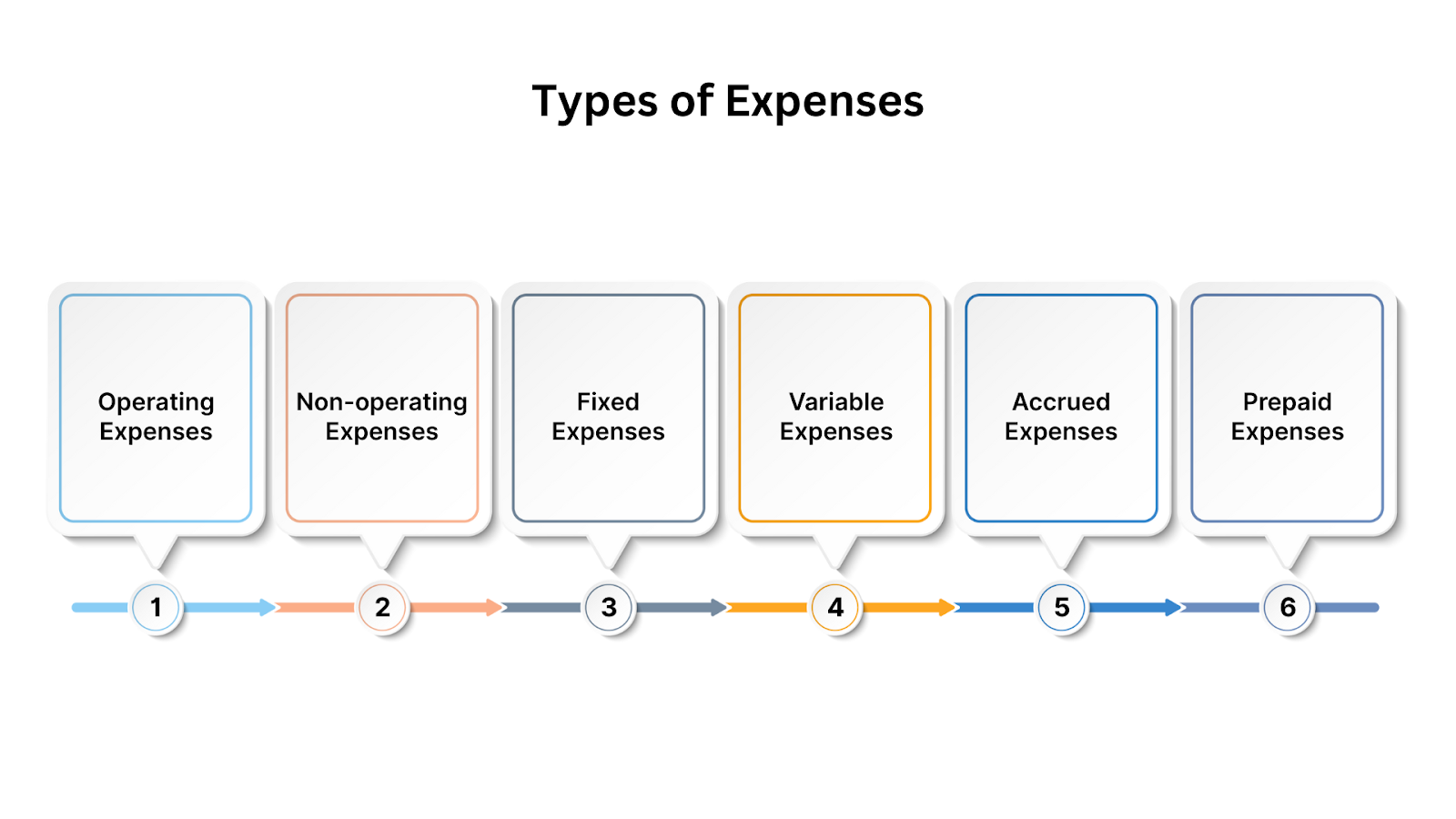

Understanding different types of expenses can significantly improve your financial management. Below are the main types of expenses businesses typically encounter:

Operating expenses are the costs associated with running the core operations of a business. These include:

These expenses are necessary for day-to-day operations but do not directly contribute to producing goods or services.

Non-operating expenses are not related to the core activities of a business. They include:

These are indirect costs that do not affect the direct production of goods or services.

Fixed expenses remain constant regardless of the company’s production levels. Examples include:

Fixed costs are predictable and stable over time, making them easier to budget for.

Variable expenses fluctuate depending on the level of production or business activity. Examples include:

These expenses rise or fall in line with the volume of sales or production output.

Accrued expenses are expenses that a business has incurred but has not yet paid. Examples include:

These expenses are recorded in the accounting period in which they occur, even if payment has not yet been made.

Prepaid expenses are payments made in advance for services or goods that will be consumed in the future. Examples include:

These are initially recorded as assets and expensed over time.

Also Read: Cost Accounting: Definition, Concepts, Types, and Uses

Once we have categorized expenses, it’s essential to understand how these are recorded in accounting to maintain accurate financial statements.

In accounting, expenses are typically recorded using the accrual basis of accounting, which means that expenses are recognized when they are incurred, not when payment is made. This ensures that the financial statements reflect the actual economic activity of a business during a given period. Here’s a more detailed breakdown of how expenses are recorded:

Following these accounting methods ensures that businesses are accurately tracking expenses and properly reporting them in their financial statements, whether using the accrual method or the cash method.

Also Read: Understanding Debits and Credits in Accounting

With a clearer understanding of how expenses are recorded, let’s explore a practical example to see how these principles are applied in a real-world setting.

To better understand how expenses are recorded in a large corporation, let’s examine an example from Saudi Aramco’s 2024 consolidated financial statements, one of the world’s leading energy companies:

Having explored the practical example of Aramco’s expense management, let's now look at how HAL ERP can help businesses optimize expense recording and VAT management.

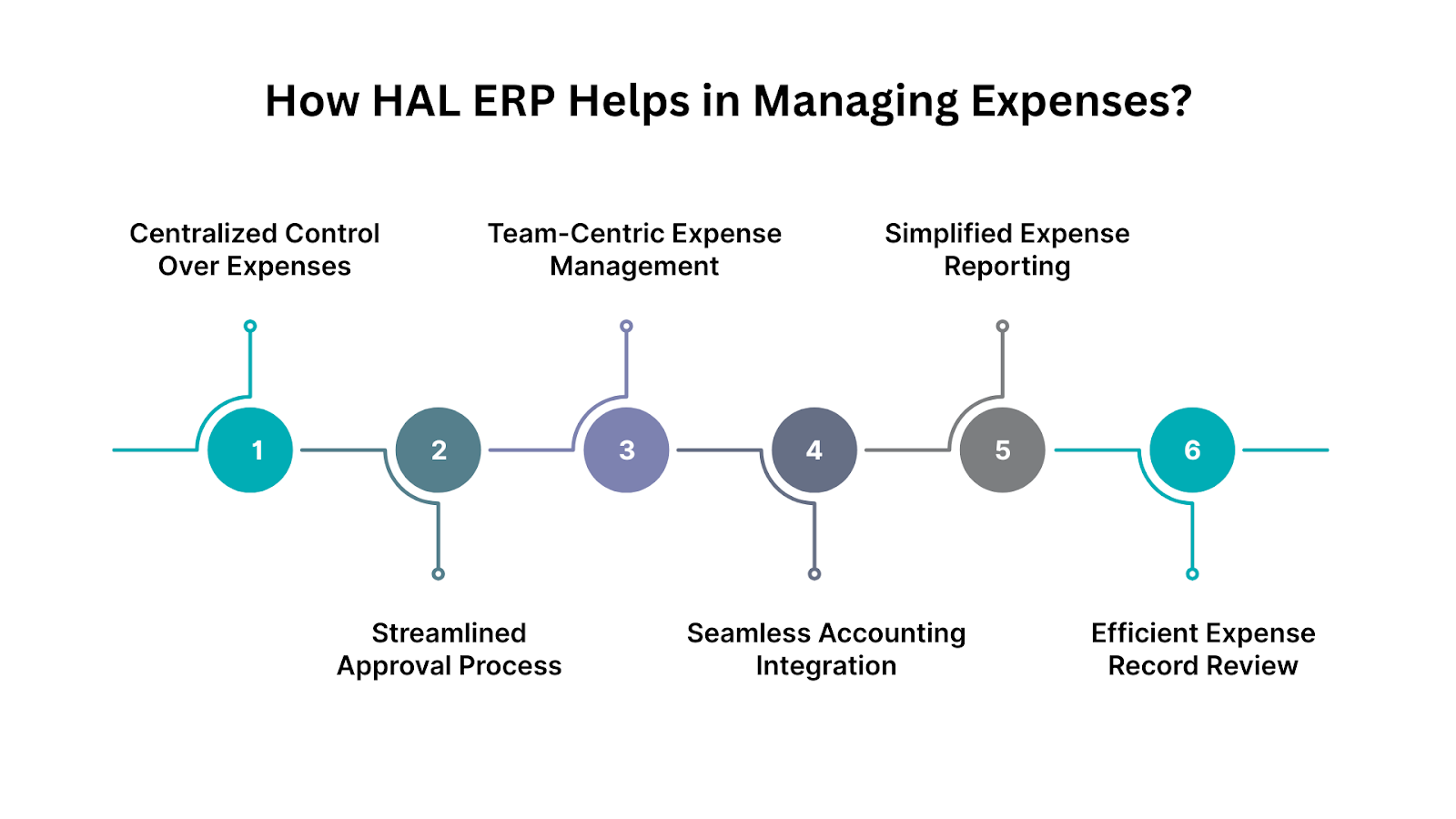

HAL ERP streamlines expense management by integrating control into every step of the process, from receipt tracking to final approval. The system allows businesses to manage and review employee expenses efficiently, ensuring seamless processes and financial compliance. Here's how HAL ERP enhances expense management:

1. Centralized Control Over Expenses:

2. Streamlined Approval Process:

3. Team-Centric Expense Management:

4. Seamless Accounting Integration:

5. Simplified Expense Reporting:

6. Efficient Expense Record Review:

Also Read: ERP Implementation Success Stories: Real-World Examples

By centralising expense management and automating key processes, HAL ERP ensures that businesses can manage employee spends efficiently, maintain compliance, and enhance financial decision-making with ease.

Understanding expenses is crucial for managing business finances and making informed decisions. By categorising and properly recording expenses, businesses can improve their profitability, stay compliant with tax regulations, and achieve financial goals. Using technology like HAL ERP can make this process seamless, ensuring that all expenses are recorded accurately and efficiently.

Explore how HAL ERP can enhance your accounting and expense management today. Book a demo and optimise your business operations!

1. What qualifies as a business expense?

Business expenses are ordinary and necessary costs incurred to run operations—such as rent, utilities, wages, depreciation, and office supplies .

2. Which expenses are tax deductible?

Only expenses that are both ordinary and necessary within your business can be deducted. Costs like lobbying, personal living expenses, or fines are generally non-deductible .

3. How do capital expenditures differ from revenue expenses?

Capital expenditures (CapEx) are investments in long‑term assets (e.g. machinery) and are capitalized, whereas revenue or operational expenses (OpEx) are day-to-day costs like utilities and are fully expensed in the period they occur

4. Which commonly missed deductions should I watch out for?

Items like continuing education, professional memberships, SaaS subscriptions, mileage for business use, and startup costs are often forgotten but potentially deductible .

5. How can expense tracking improve financial health?

Tracking expenses rigorously supports better cash flow management, tax preparation, audit readiness, budgeting, and profitability analysis. It’s a core function of financial discipline .