Month End Closing Process: Core Components and Steps

Published By

Umar Shariff

General Accounting

Apr 2, 2026

Month-end closing determines how much the business can trust its numbers. When the close runs late, decision-making slows down, reconciliations get rushed, and small gaps turn into last-minute adjustments that are harder to explain and easier to repeat next month.

Global benchmarking from APQC’s General Accounting Open Standards survey shows a clear performance gap: the median close cycle time is 6.4 calendar days, top performers close in 4.8 days or less, and the bottom quartile takes 10+ days.

This guide shows you how to run an accurate month-end closing process with a step-by-step approach and a practical checklist, so you can make your close predictable, controlled, and audit-ready.

Key Takeaways

A structured month-end closing process improves financial accuracy, reduces last-minute adjustments, and strengthens management confidence in reported results.

Closing subledgers, applying accruals, reconciling high-risk accounts, and locking the period in the correct sequence prevents recurring reporting errors.

Accuracy during close directly impacts VAT compliance, audit readiness, and decision-making reliability for mid-sized Saudi enterprises.

Measuring KPIs such as days to close, reconciliation completion rate, and manual journal volume helps finance teams identify control gaps and improve predictability.

ERP automation reduces reconciliation delays, manual posting risk, and compliance pressure by synchronizing operational and financial data in real time.

What Is the Month-End Closing Process?

The month-end closing process is the structured set of accounting activities performed at the end of each month to ensure all financial transactions are recorded accurately and completely. It confirms that revenues, expenses, assets, and liabilities are properly recognized before financial statements are finalized.

The objective is simple: produce reliable financial reports that reflect the true position of the business for that period.

For Saudi enterprises, month-end close carries additional weight. Financial statements must align with VAT calculations, support ZATCA e-invoicing records, and withstand audit scrutiny. When the close is rushed or inconsistent, the risk is not only internal misreporting. It can affect compliance, tax accuracy, and management credibility.

Core Components of a Month-End Closing Process

A reliable month-end closing process follows a defined structure. Each component builds on the previous one, reducing the chance of rework and late adjustments.

1. Subledger Finalization

Accounts receivable, accounts payable, payroll, inventory, and fixed assets must be closed before the general ledger is reviewed. This ensures all operational transactions for the month are captured.

2. Accruals and Adjusting Entries

Expenses incurred but not yet invoiced, prepaid allocations, depreciation, and revenue recognition entries are recorded based on accounting policy. This step aligns financial results with actual economic activity, not just cash movement.

3. Bank and Cash Reconciliation

Book balances are matched against bank statements. Any unmatched items are investigated and resolved to confirm cash accuracy.

4. Balance Sheet Reconciliations

High-risk accounts such as receivables, payables, inventory, taxes, loans, and intercompany balances are reconciled against supporting schedules. No balance should remain unexplained.

5. Inventory and Cost Validation

Stock movements, valuation methods, and cost of goods sold are reviewed to confirm cut-off accuracy and prevent margin distortion.

6. Analytical Review

Financial results are compared against prior periods and budgets. Unexpected variances are investigated before reports are finalized.

7. Financial Statement Preparation and Period Locking

Once validated, the income statement, balance sheet, and cash flow statement are generated. The accounting period is then locked to prevent backdated changes.

Understanding the structure of a close explains how it works. But structure alone is not enough. The real question is what happens when accuracy breaks down, and why precision at every stage matters.

How Does Accuracy in Month-End Closing Impact Financial Control?

An accurate month-end close determines whether leadership is working with facts or assumptions. When numbers are incomplete or misclassified, reporting delays follow, adjustments increase, and confidence in financial statements weakens.

Here’s why precision during close matters:

Reliable financial reporting: Accurate closing ensures the income statement and balance sheet reflect actual performance, not timing gaps or posting errors.

Stronger regulatory and VAT compliance: Clean reconciliations and properly recorded transactions reduce risk during audits and support accurate VAT reporting aligned with ZATCA requirements.

Faster, better decision-making: Management can act on margin trends, cost movements, and revenue performance without waiting for corrections or revised reports.

Improved cash flow visibility: Confirmed receivables, payables, and bank balances give a clear view of working capital and liquidity.

Early detection of errors and anomalies: Structured reconciliation and variance review identify duplicate entries, missing accruals, and unusual activity before they compound.

Reduced month-to-month volatility: When the close is disciplined, last-minute adjustments decline, and financial results become more predictable.

Accuracy during close protects operational stability, compliance posture, and executive confidence in the numbers.

Once the importance of accuracy is clear, the focus shifts to execution. The difference between a stable close and a chaotic one often lies in the discipline of the process itself.

Step-by-Step Month-End Closing Process

A reliable month-end close is built on sequence and control. Each step reduces uncertainty before moving to the next. When teams follow a consistent structure, they prevent reconciliation breaks, reduce last-minute adjustments, and shorten review cycles.

The framework below outlines what finance teams should execute, in order, to maintain reporting accuracy and audit readiness:

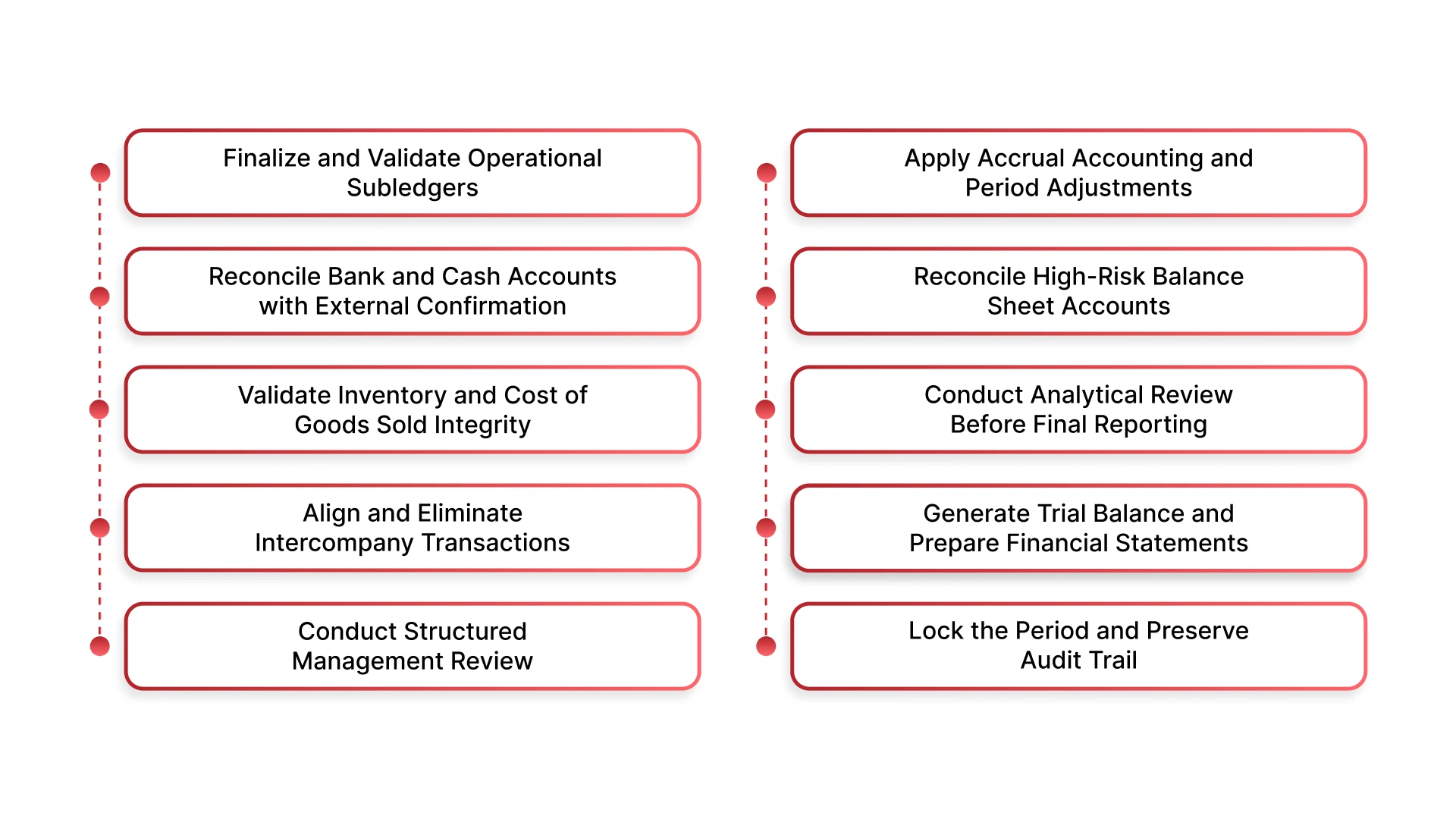

Step 1: Finalize and Validate Operational Subledgers

The general ledger cannot be trusted if the systems feeding it are incomplete. Subledgers represent real operational activity. If they are not fully posted, reconciled, and reviewed, every financial statement derived from them becomes questionable.

Before moving forward, confirm operational completeness.

Execute the following:

Confirm all customer invoices for the month are issued, posted, and reflected in AR aging

Ensure all supplier invoices are recorded, approved, and not sitting in pending queues

Complete payroll processing and verify related liabilities are posted

Record all inventory movements including goods receipts, transfers, returns, and adjustments

Update fixed asset additions, disposals, and capitalization entries

Validate that:

No backlogs remain in transactional systems

Cut-off dates are enforced consistently across departments

Revenue and expense recognition aligns with the correct period

This step prevents late discoveries that force reopening reconciliations later.

Step 2: Apply Accrual Accounting and Period Adjustments

Accruals are where accounting discipline shows. Without structured accrual logic, profits shift unpredictably between months. That volatility reduces management confidence and complicates performance analysis.

This stage ensures economic reality is reflected.

Execute the following:

Record accrued expenses for utilities, rent, services, and contracts not yet invoiced

Adjust prepaid expenses to reflect the portion consumed in the month

Recognize revenue according to milestone completion or delivery status

Post depreciation and amortization based on approved asset schedules

Record provisions or estimated liabilities where required

Validate that:

Adjustments follow documented accounting policy

Recurring accruals use standardized templates

All entries have supporting documentation and reviewer approval

Balance sheet reconciliation is where many close processes break down. Unreconciled accounts often carry errors forward month after month.

Focus on accounts with financial or compliance sensitivity.

Execute the following:

Tie accounts receivable to detailed aging reports

Match accounts payable to supplier statements

Confirm inventory balances align with stock and valuation records

Reconcile VAT payable and recoverable balances

Validate intercompany receivables and payables

Confirm loan balances against repayment schedules

Validate that:

Every account has a supporting schedule

Differences are identified, explained, and resolved

No material balances remain unexplained

This step protects against cumulative misstatements.

Step 5: Validate Inventory and Cost of Goods Sold Integrity

Inventory directly affects margins. Errors here distort profitability and can mislead management decisions.

Inventory validation is not just a quantity check. It is a cost integrity review.

Execute the following:

Confirm correct cut-off for goods received and shipped

Validate that the chosen valuation method is applied consistently

Review write-offs, shrinkage, and obsolete stock adjustments

Confirm production cost allocations if manufacturing applies

Compare system records with physical stock counts where required

Validate that:

COGS aligns with actual movement

Gross margin movements are explainable

No timing distortions inflate or deflate profit

Inventory review often reveals operational process gaps.

Step 6: Conduct Analytical Review Before Final Reporting

After technical reconciliations, perform financial reasonableness testing. This is where patterns matter more than transactions.

Analytical review surfaces anomalies that transactional checks may miss.

Execute the following:

Compare month-over-month revenue trends

Analyze budget versus actual performance

Review gross margin fluctuations

Identify unusual cost spikes

Scan for duplicate or misclassified entries

Validate that:

Significant variances are explained with supporting logic

Margin shifts align with operational changes

No abnormal movements remain uninvestigated

This step converts accounting accuracy into management insight.

Step 7: Align and Eliminate Intercompany Transactions

For multi-entity groups, intercompany mismatches distort consolidated reporting. Alignment at this stage prevents reporting inconsistencies later.

Execute the following:

Match intercompany receivables and payables across entities

Confirm internal cost allocations and recharge logic

Prepare elimination entries for consolidation

Resolve timing differences

Validate that:

Balances match across both sides of the transaction

No unexplained discrepancies remain before consolidation

Without this discipline, group reporting becomes unreliable.

Step 8: Generate Trial Balance and Prepare Financial Statements

Once validations are complete, produce the formal outputs.

The trial balance acts as the final structural integrity check.

Execute the following:

Run trial balance and confirm debits equal credits

Review unusual account movements

Prepare income statement, balance sheet, and cash flow

Generate variance commentary for management

Validate that:

Statements reflect reconciled balances

Adjustments are properly captured

Financial outputs are internally consistent

At this point, numbers should require explanation, not correction.

Step 9: Conduct Structured Management Review

This stage shifts from accounting control to business validation.

Leadership review should focus on trends, not basic accuracy.

Execute the following:

Review revenue growth consistency

Assess cost movement drivers

Validate margin stability

Examine high-value journal entries

Confirm compliance-sensitive balances

Validate that:

Explanations are documented

Adjustments are approved formally

Reporting reflects business reality

This prevents surprises during audit or board review.

Step 10: Lock the Period and Preserve Audit Trail

Closing is incomplete until the system enforces stability.

Period locking protects reporting integrity.

Execute the following:

Lock the accounting period in the system

Disable backdated postings

Archive reconciliation schedules

Retain documentation for audit review

Validate that:

Reports remain stable after sign-off

No post-close modifications occur without approval

A locked period ensures that next month starts clean.

A defined process improves control, but improvement should be measurable. To understand whether the close is truly becoming faster and more reliable, performance needs to be tracked with clear metrics.

KPIs to Measure Closing Efficiency

Tracking the right KPIs helps you measure whether close is getting faster, cleaner, and more predictable. These metrics also make it easier to identify where delays and errors originate.

KPI

How to Calculate?

What It Helps Measure?

Days to Close

Final Close Date − Period End Date

Overall close speed and where delays occur across phases.

Number of Adjustments

Count of journal entries posted after first draft financials

Quality of upstream postings and effectiveness of cut-off controls.

Reconciliation Completion Rate

(Number of Reconciled Accounts ÷ Total Priority Accounts) × 100

Coverage and discipline of balance sheet control before reporting.

Error Rate

(Number of Identified Errors ÷ Total Transactions or Journal Entries) × 100

Posting accuracy, control effectiveness, and process reliability.

Manual Journal Entry Count

Total Manual Journal Entries Posted During Close

Level of automation and exposure to manual error risk.

Close Cycle Consistency

Standard Deviation of Days to Close over 6–12 Months

Stability and predictability of the closing process month to month.

KPIs show performance trends. A checklist ensures control discipline. Before locking the period, finance teams need a structured validation layer to confirm stability and compliance.

Month-End Close Control Validation Checklist

A month-end checklist should function as a control validation tool, not a task tracker. Its purpose is to confirm that financial data is complete, reconciled, supported, and approved before the period is locked.

Each element below focuses on verification points that reduce reporting risk, audit exposure, and recurring month-to-month errors.

Control Area

What to Verify

Risk If Not Confirmed

Cut-Off Discipline

All departments confirmed transaction cut-off

No backdated postings after review

Revenue and expense recognition align with policy

Revenue or expenses recorded in the wrong period, distorting profit

Subledger Integrity

AR and AP aging reports tie to GL

Inventory subledger matches control account

Payroll liabilities reconcile to HR records

GL balances unreliable due to subledger mismatch

Accrual Completeness

Standard recurring accruals posted

One-off accruals reviewed

Supporting documentation attached

Prior-month accrual reversals verified

Understated expenses or overstated profits

Cash Accuracy

Bank reconciliations completed and reviewed

No unexplained reconciling items

Old outstanding items cleared or justified

Misstated cash balances and audit exposure

Balance Sheet Support

Every material balance has a supporting schedule

Variances are documented and resolved

Suspense accounts reviewed and minimized

Errors carry forward and compound month to month

Inventory & COGS Reliability

Valuation method applied consistently

Cut-off confirmed for goods received/shipped

Write-offs approved and recorded

Margin distortion and profitability misstatement

VAT & Compliance Alignment

VAT payable/recoverable reconciled

E-invoicing records align with reported sales

Compliance-sensitive balances reviewed

Regulatory exposure and reporting penalties

Intercompany Accuracy (if applicable)

Intercompany balances match across entities

Eliminations prepared and reviewed

Transfer pricing consistent

Consolidated reporting inconsistencies

Analytical Review Completion

Major variances investigated

Margin movement explained

Unusual entries justified

Undetected misclassifications or operational anomalies

Journal Entry Control

Manual journal entries reviewed and approved

High-value entries examined

No unsupported adjustments remain

Weak audit trail and higher fraud risk

Documentation & Audit Trail

Reconciliation files archived

Approval evidence retained

Period formally locked in system

Audit delays and loss of reporting integrity

Management Sign-Off

Financial statements reviewed

Commentary prepared

Formal approval recorded

Lack of accountability and governance gaps

If your month-end close still depends on spreadsheets, manual reconciliations, and last-minute corrections, ERP automation can remove that pressure.

This is where system design becomes critical. The right ERP enforces control, synchronizes data, and reduces close volatility at the source.

How Does HAL ERP Strengthen and Accelerate Your Month-End Close?

Month-end pressure usually comes from fragmentation. Disconnected systems. Manual reconciliations. Late adjustments. HAL ERP is built to eliminate those gaps by centralizing finance, operations, compliance, and reporting into one controlled environment designed for Saudi enterprises.

Here’s how HAL directly improves close stability and speed:

Real-Time Subledger Synchronization: Sales, procurement, payroll, and inventory post directly into the general ledger without re-entry. Finance teams work with live numbers, not delayed exports.

Automated Journal Entries and Policy-Based Posting: Recurring accruals, depreciation, revenue recognition, and allocations are standardized and system-driven, reducing manual journals and approval bottlenecks.

AI-Assisted Bank Reconciliation: HAL’s reconciliation tools match transactions automatically and surface only exceptions for review, cutting hours from cash validation.

Integrated VAT and ZATCA Alignment: E-invoicing records, VAT calculations, and financial reporting stay aligned within the same system, reducing compliance exposure and last-minute filing stress.

Multi-Entity and Intercompany Control: Automated intercompany postings and unified reporting simplify consolidation while maintaining company-level data control.

Inventory and Cost Visibility in Real Time: Accurate valuation, COGS updates, and stock movement tracking reduce margin volatility during close.

Conversational Reporting with HALA: Finance leaders can pull trial balances, variance reports, or account summaries instantly through WhatsApp, accelerating review cycles without waiting on manual report preparation.

Structured Period Lock and Audit Trail: Role-based access, approval workflows, and system locking prevent unauthorized backdated changes and protect reporting integrity.

Fast Implementation with Dedicated Transition Teams: Basic finance setup can be completed in 2–4 weeks, with full implementation including migration and customization typically delivered within 8–12 weeks, minimizing operational disruption.

HAL ERP is not just accounting software. It is a controlled financial operating system built for enterprises that need compliance, visibility, and predictable reporting cycles.

If your month-end close still feels reactive, schedule a demo with HAL and map the platform directly to your current finance workflow.

Conclusion

An accurate month-end closing process is essential for financial control and business visibility. With a structured step-by-step workflow and a standardized checklist, teams can reduce errors, shorten close cycles, and deliver reporting that leadership can trust month after month.

If your close is still heavily manual or dependent on spreadsheets, an ERP-led finance workflow can help automate postings, streamline reconciliations, and improve audit readiness.

To see how HAL ERP can support a faster, more controlled month-end close, book a demo and map the platform to your current close process.

FAQs

1. How do you identify bottlenecks in your month-end closing process?

Review phase-level timelines rather than total days to close. If subledgers, reconciliations, or management review consistently exceed target timelines, those stages likely contain process gaps or manual dependencies.

2. Should month-end closing responsibilities be centralized or distributed?

A hybrid model works best. Operational teams confirm transactional completeness, while finance maintains ownership of reconciliations, adjustments, and final approval to preserve control and accountability.

3. How often should the month-end closing process itself be reviewed or updated?

At least annually, or after major system changes, new regulatory requirements, or organizational restructuring. A static close process often fails to adapt to operational growth.

4. What documentation should be retained for audit readiness?

Reconciliation schedules, journal entry support, approval evidence, cut-off confirmations, and period lock confirmation should all be archived systematically to ensure traceability.

5. How does close discipline impact long-term financial planning?

Consistent and accurate monthly closes improve forecast reliability, reduce variance surprises, and strengthen budgeting accuracy over time.

Umar Shariff

Umar Shariff is a serial entrepreneur and CEO of HAL Simplify, celebrated for making ERP platforms seamless and intuitive for Middle Eastern organizations. With extensive experience scaling team and driving digital transformation projects in Saudi Arabia with accelerated deployment, Umar excels at operational management, team leadership, and delivering future-ready ERP systems that elevate regional business performance.